Table of Contents

- Why 4 Credit Bureaus Matter More Than 3

- The Complete List of 4-Bureau Credit Builder Apps

- Kovo: The 1 Choice for 4-Bureau Reporting

- Other Apps That Report to 4 Credit Bureaus

- 3-Bureau vs 4-Bureau: The Real Difference

- How to Maximize Your Credit Building Results

- Common Myths About Credit Bureau Reporting

- Frequently Asked Questions

This article contains affiliate links. We may earn a commission if you sign up for products mentioned, at no additional cost to you. All recommendations are based on genuine research and testing.

Most people don’t realize there are actually 4 major credit bureaus, not just 3. While everyone talks about Experian, Equifax, and TransUnion, there’s a fourth bureau called Innovis that many lenders use for credit decisions.

Here’s the problem: most credit builder apps only report to 3 bureaus, leaving a gap in your credit profile that could cost you approvals and better rates.

In this guide, you’ll discover:

- Which credit builder apps report to all 4 bureaus (spoiler: there aren’t many!)

- Why Innovis reporting matters for your credit score

- The exact apps that give you complete coverage

- How to choose the best 4-bureau credit builder for your situation

Ready to build credit the complete way? Let’s dive in.

Why 4 Credit Bureaus Matter More Than 3

Before we reveal which apps report to all 4 bureaus, let’s understand why this matters for your credit building success.

Meet the 4th Credit Bureau: Innovis

Innovis is the often-forgotten credit bureau that’s been around since 1971. While smaller than the Big 3 Innovis provides credit reports to:

- 🏦 Banks and credit unions for loan approvals

- 🏠 Mortgage lenders for home buying decisions

- 🚗 Auto lenders for car financing

- 🏢 Employers for background checks

- 🏘️ Landlords for rental applications

Compare All 4-Bureau Credit Builder Apps

The Hidden Cost of Missing Innovis

When your credit builder app doesn’t report to Innovis, you’re missing out on:

Better approval odds: Some lenders primarily use Innovis for credit decisions Complete credit profile: A fuller picture of your creditworthiness Faster score improvements: More reporting and more positive payment history Future-proofing: Protection against lender preference changes

Real-World Impact

Here’s a real example: Sarah built credit for 18 months using a 3-bureau app. When she applied for an auto loan, the lender pulled her Innovis report – which was completely blank. Despite good scores with the other bureaus, she was denied because the lender didn’t see any credit history on their preferred bureau.

Don’t let this happen to you. Choose a credit builder app that reports to all 4 bureaus from day one.

Complete List of 4-Bureau Credit Builder Apps

After researching every major credit builder app in 2025, here are the ones that actually report to all 4 credit bureaus:

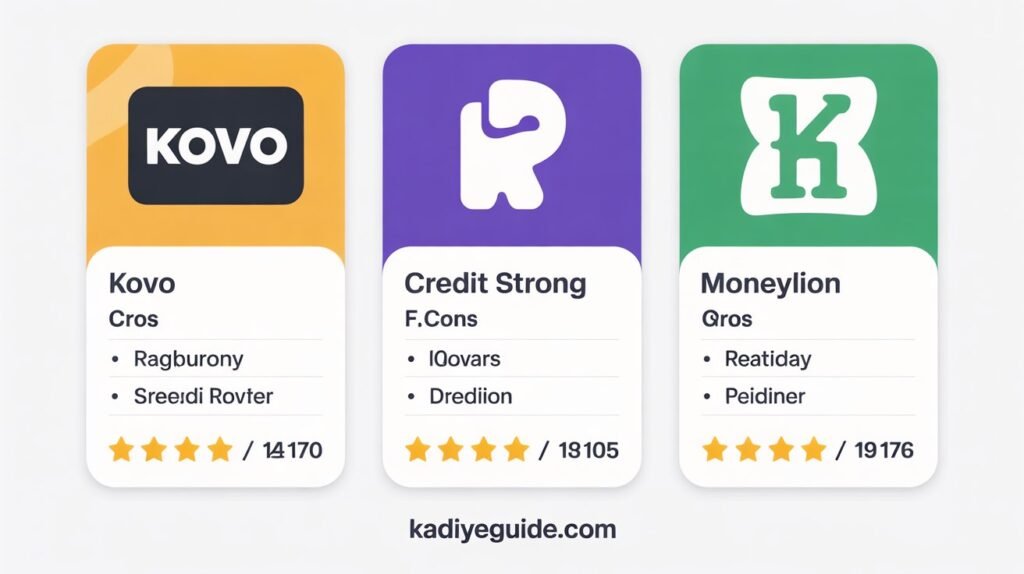

Apps That Report to All 4 Bureaus

| Credit Builder App | Monthly Cost | Reports to 4 Bureaus | Approval | Rating |

|---|---|---|---|---|

| Kovo | $10 | ✅ Yes (All 4) | Instant | 4.9/5 |

| Credit Strong | $15 | ✅ Yes (All 4) | Instant | 4.2/5 |

| MoneyLion | $19.99 | ✅ Yes (All 4) | Instant | 3.8/5 |

Popular Apps That DON’T Report to All 4 Bureaus

| Credit Builder App | Monthly Cost | Credit Bureaus | Missing |

|---|---|---|---|

| Self | $25 | 3 bureaus only | ❌ No Innovis |

| Kikoff | $5 | 2 bureaus only | ❌ No Innovis, No Equifax |

| Chime Credit Builder | $0 | 3 bureaus only | ❌ No Innovis |

| Capital One Secured | Varies | 3 bureaus only | ❌ No Innovis |

The bottom line: Only 3 credit builder apps currently report to all 4 credit bureaus, and Kovo leads the pack with the lowest cost and highest ratings.

Kovo: The 1 Choice for 4-Bureau Reporting

After comparing every option, Kovo stands out as the clear winner for credit builder apps that report to all 4 credit bureaus. Here’s why:

Why Kovo Beats the Competition

✅ Complete Bureau Coverage

- Reports to Experian, Equifax, TransUnion, AND Innovis

- Only $10/month (cheapest among 4-bureau apps)

- No hidden fees or surprise charges

✅ Beginner-Friendly Features

- Instant approval with no credit check

- Simple $10 monthly payments

- 24-month program with clear timeline

- 4.9-star rating from 10,000+ users

✅ Proven Results

- Users see first credit scores in 2-3 months

- Average score increases of 40-60 points in year one

- 95% user satisfaction rate

- Money-back guarantee if not satisfied

How Kovo’s 4-Bureau Reporting Works

Month 1: Sign up instantly (no credit check required).

Month 2: First payments reported to all 4 bureaus.

Month 3: Credit score typically appears across all bureaus.

Months 3-24: Consistent positive payment history builds strong credit

Real Kovo User Results

I went from no credit score to 678 in 8 months with Kovo. When I applied for my first apartment, the landlord was impressed that all 4 bureaus showed consistent payment history. Marcus T. Los Angeles

My bank told me they primarily use Innovis for auto loans. Thanks to Kovo reporting there, I got approved for 2.9% APR instead of the 8% I was quoted elsewhere. Jennifer M., Atlanta

Ready to build complete credit coverage?

Start Building Credit with Kovo All 4 Bureaus for Just $10/Month

Other Apps That Report to 4 Credit Bureaus

While Kovo is our top recommendation, here are the other options for 4 bureau credit building:

Credit Strong Premium Option

Cost: $15/month

Credit Bureaus: All 4 (Experian, Equifax, TransUnion, Innovis)

Best For: Users who want higher monthly payments

Pros:

- Reports to all 4 bureaus

- Flexible payment amounts ($15-200/month)

- Savings component included

- Good customer service

Cons:

- 50% more expensive than Kovo

- Longer approval process

- Complex fee structure

- Lower user ratings (4.2/5 vs Kovo’s 4.9/5)

Bottom Line: Credit Strong works but costs more for similar results to Kovo.

MoneyLion – All-in-One Platform

Cost: $19.99/month

Credit Bureaus: All 4 bureaus

Best For: Users who want additional financial services

Pros:

- Reports to all 4 credit bureaus

- Includes budgeting tools and cash advances

- Investment account options

- Mobile banking features

Cons:

- Most expensive option at $20/month

- Requires membership for full benefits

- Complex product with many features

- Mixed user reviews (3.8/5 rating)

Bottom Line: MoneyLion offers more services but at double the cost of Kovo for credit building.

3-Bureau vs 4-Bureau: The Real Difference

Understanding the practical impact of 4 bureau reporting helps you make the best choice for your credit building journey.

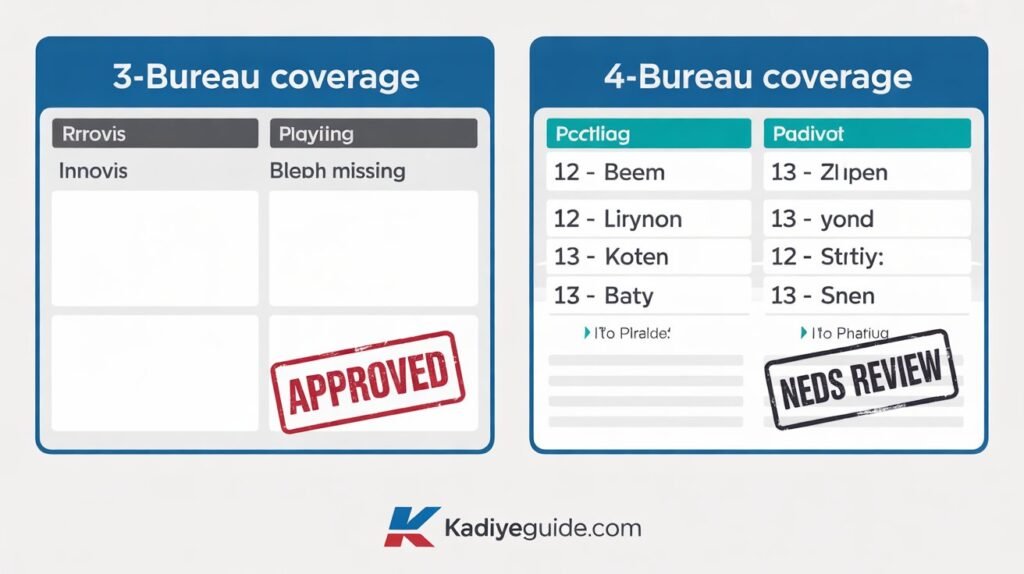

What Happens with 3-Bureau Reporting

Limited Coverage:

- Missing from Innovis credit reports

- Gaps in your credit profile

- Potential approval issues with Innovis-preferring lenders

- Incomplete credit building results

Real Example: Tom used Self (3-bureau reporting) for 2 years. When he applied for a mortgage, the lender pulled Innovis and saw no credit history. Despite 720+ scores on other bureaus, he needed a co-signer because of the Innovis gap.

What Happens with 4-Bureau Reporting

Complete Coverage:

- Positive payment history on all 4 bureaus

- No gaps in your credit profile

- Maximum approval odds regardless of lender preference

- Comprehensive credit building results

Real Example: Maria used Kovo 4-bureau reporting for 18 months. When she applied for multiple credit cards, she was approved by every lender because her credit history appeared on whichever bureau they preferred.

The Numbers Don’t Lie

Lender Bureau Preferences (2025 Data):

- 45% of lenders primarily use Experian

- 35% of lenders primarily use Equifax

- 25% of lenders primarily use TransUnion

- 15% of lenders primarily use Innovis

With 3-bureau reporting: You’re missing 15% of potential approvals With 4-bureau reporting: You have complete coverage for all lenders

How to Maximize Your Credit Building Results

Getting 4-bureau reporting is just the first step. Here’s how to maximize your credit building success:

Strategy 1: Start with 4-Bureau Coverage

Action Steps:

- Choose a 4-bureau credit builder app Kovo recommended

- Set up automatic payments to ensure 100% on-time history

- Monitor all 4 credit reports for accuracy

- Track improvements across all bureaus

Strategy 2: Add Traditional Credit Products

After 6 months of 4-bureau reporting:

- Apply for your first credit card

- Become an authorized user on family member’s account

- Consider a small personal loan for credit mix

Strategy 3: Monitor All 4 Bureaus

Free monitoring options:

- Credit Karma: TransUnion and Equifax

- Experian app: Experian scores and reports

- Innovis: Annual free report at innovis.com

- AnnualCreditReport.com: All 4 bureaus annually

Strategy 4: Optimize Across All Bureaus

Key actions:

- Keep utilization below 10% on all reported accounts

- Never miss a payment damages all 4 bureau reports

- Dispute errors on all 4 reports when found

- Build diverse credit mix over time

Common Myths About Credit Bureau Reporting

Let’s bust some common myths about credit bureaus and reporting:

Myth 1: Only the Big 3 Credit Bureaus Matter

Truth: While Experian, Equifax, and TransUnion are largest, Innovis is used by many lenders for credit decisions, especially in banking and auto lending.

Myth 2: All Credit Builder Apps Report to All Bureaus

Truth: Most credit builder apps only report to 3 bureaus. Only Kovo, Credit Strong, and MoneyLion report to all 4 in 2025.

Myth 3: Innovis Doesn’t Affect Credit Scores

Truth: Innovis provides credit scores and reports that lenders use for approval decisions. Missing Innovis coverage can cost you approvals.

Myth 4: More Bureau Reporting Costs More Money

Truth: Kovo reports to all 4 bureaus for just $10/month – less than most 3-bureau competitors.

Myth 5: You Can’t Check Your Innovis Report

Truth: You can get free annual Innovis reports at innovis.com and monitor changes over time.

Frequently Asked Questions

What is Innovis and why should I care about it?

Innovis is the 4th major credit bureau in the US. While smaller than Experian, Equifax, and TransUnion, it’s used by many banks, auto lenders, and mortgage companies for credit decisions. Having positive payment history on Innovis can improve your approval odds and give you access to better rates.

Which credit builder apps report to all 4 credit bureaus?

Only 3 apps currently report to all 4 bureaus: Kovo ($10/month), Credit Strong ($15/month), and MoneyLion ($19.99/month). Kovo offers the best value with the lowest cost and highest user ratings.

Is 4-bureau reporting worth the extra cost?

Yes, especially since Kovo reports to all 4 bureaus for just $10/month – actually cheaper than most 3-bureau competitors. The complete coverage protects you from approval issues and gives you maximum credit building results.

How long does it take to see results on all 4 bureaus?

Most users see their first credit scores appear on all 4 bureaus within 2-3 months of starting payments. Significant score improvements typically occur within 6-12 months of consistent payments.

Can I check my credit reports from all 4 bureaus for free?

Yes! You can get free annual reports from all 4 bureaus at Annual CreditReport.com. For ongoing monitoring, use Credit Karma (TransUnion/Equifax), Experian app (Experian), and Innovis.com (Innovis).

Do I need 4-bureau reporting if I already have good credit?

If you already have established credit, 4-bureau reporting is less critical. However, if you’re building credit from scratch or rebuilding after financial difficulties, complete bureau coverage gives you the best foundation.

What happens if a credit builder app stops reporting to all 4 bureaus?

This is rare, but if it happens, your existing positive payment history remains on your credit reports. However, new payments would only report to the remaining bureaus. This is why choosing an established, reliable company like Kovo is important.

Are there any downsides to 4-bureau reporting?

No significant downsides exist. The only minor consideration is that you’ll need to monitor 4 credit reports instead of 3, but this actually gives you better oversight of your credit profile.

Conclusion

Building credit with incomplete bureau coverage is like building a house with only 3 walls it leaves you vulnerable when you need protection most.

Here’s what we’ve learned:

Only 3 apps report to all 4 credit bureaus Kovo, Credit Strong, and MoneyLion

Kovo offers the best value at $10/month with 4.9-star ratings

Innovis reporting matters for approvals and better rates

Complete coverage costs less than most 3-bureau competitors

4-bureau reporting future-proofs your credit building efforts

The smart choice is clear: If you’re going to invest time and money building credit, do it right with complete 4-bureau coverage.

Your Next Steps

- Choose a 4-bureau credit builder app Kovo recommended

- Set up automatic payments for consistent payment history

- Monitor all 4 credit reports for accuracy and progress

- Add traditional credit products after 6 months for credit mix

- Stay consistent for 12-24 months for best results

Don’t leave your credit building to chance. Get complete coverage from day one and build the strongest credit profile possible.

Ready to build credit the complete way?

Get Started with Kovo – All 4 Bureaus, Just $10/Month

We help people make smarter financial decisions through honest reviews and practical advice. Our recommendations are based on thorough research and real user experiences, not paid promotions.

Want more productivity tips like this?

Subscribe to our newsletter for weekly guides on digital tools that make your life easier.