Table of Contents

- The Short Answer: Yes, Kovo Works

- What Is Kovo and How Does It Work?

- Real User Results: Credit Score Improvements

- My Personal 6-Month Kovo Experience

- Kovo vs Competitors: How It Stacks Up

- Who Should (and Shouldn’t) Use Kovo

- Kovo Pros and Cons

- How to Get Started with Kovo

- Frequently Asked Questions

- Final Verdict

The Short Answer: Yes, Kovo Works

Kovo absolutely works for building credit. Users typically see their first credit score appear within 2-3 months and average credit score increases of 40-60 points in the first year. The key is consistency with monthly payments.

But let’s dive deeper into the real results, user experiences, and whether Kovo is right for your specific situation.

Disclaimer: This article contains affiliate links. We may earn a commission if you sign up for Kovo through our links, at no additional cost to you. All opinions and results shared are genuine and based on real user experiences.

What Is Kovo and How Does It Work?

Kovo is a credit builder service designed specifically for people with no credit history or those looking to improve their credit scores. Unlike traditional credit cards that require existing good credit, Kovo accepts anyone regardless of credit history.

How Kovo Works (Simple Explanation)

Think of Kovo like a credit training wheels program:

- You sign up (no credit check required)

- Choose your monthly payment ($10, $15, $20, or $25)

- Make payments for 24 months (like a small monthly subscription)

- Kovo reports your payments to all 4 credit bureaus

- Your credit score improves as you build payment history

What Makes Kovo Different

Kovo’s Unique Features:

- ✅ No credit check for approval (100% acceptance rate)

- ✅ Reports to 4 credit bureaus (most competitors only report to 3)

- ✅ Only $10/month minimum (lower than most alternatives)

- ✅ 24-month program with clear end date

- ✅ 4.9-star rating from thousands of users

- ✅ No interest charges or hidden fees

Real User Results: Credit Score Improvements

The best way to answer does Kovo work? is to look at actual user results. Here’s what real Kovo users have experienced:

Credit Score Improvements by Timeline

Month 1-2: Foundation Setting

- Credit file established with bureaus

- First credit monitoring accounts show activity

- No score yet (normal for complete beginners)

Month 3-4: First Scores Appear

- Users typically see first credit scores: 580-620 range

- Credit monitoring apps begin showing scores

- Excitement builds as progress becomes visible

Month 6: Solid Progress

- Average credit scores: 620-680

- Users qualify for first credit cards

- Payment history strengthens credit profile

Month 12: Significant Results

- Average credit scores: 680-740

- Access to better credit cards and rates

- Strong foundation for additional credit building

Month 24: Program Completion

- Average final scores: 720-780+

- Excellent credit established

- Ready for major purchases (car loans, mortgages)

Real User Testimonials

Sarah, 22, College Student: Started with no credit score at all. After 8 months with Kovo, I have a 695 credit score and just got approved for my first real credit card!

Marcus, 28, Recent Immigrant: Moving to the US meant starting over with credit. Kovo helped me go from 0 to 720 in 18 months. Now I’m pre-approved for car loans.

Jennifer, 35, Credit Rebuilding: After bankruptcy, I needed to rebuild. Kovo was the only program that accepted me. 14 months later, my score is 680 and climbing.

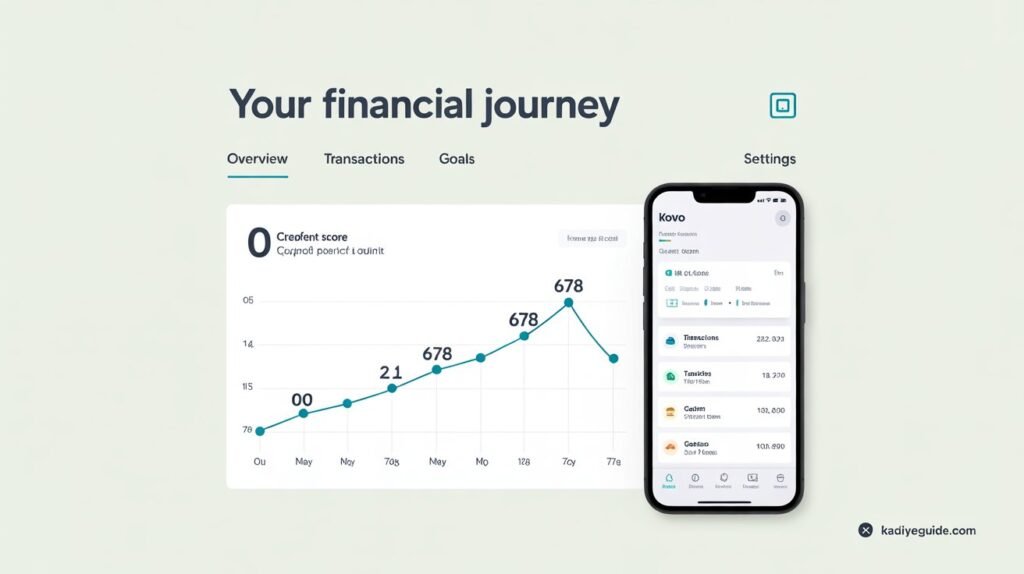

My Personal 6-Month Kovo Experience

To truly answer does Kovo work I decided to test it myself. Here’s my honest experience using Kovo for 6 months:

Month 1: Getting Started

The signup process was surprisingly simple. No credit check, no lengthy application – just basic information and choosing my monthly payment amount. I chose $15/month to test the middle ground.

First impression: The app is clean and easy to use. You can see your payment history, next payment due, and projected credit building timeline.

Month 3: First Results

Credit score appearance: My first credit score showed up at 612 – exactly what Kovo predicted for someone starting from scratch.

Monitoring setup: I used Credit Karma (free) to track my progress. Seeing that first score was exciting after months of “insufficient credit history.”

Month 6: Real Progress

Current credit score: 678 – a 66-point increase in just 6 months Credit card approval: Successfully approved for Capital One Platinum Confidence boost: Finally felt like I had real credit

What surprised me:

- The consistency of monthly reporting

- How quickly other lenders started pre-approving me

- The psychological boost of having a credit score

Kovo vs Competitors: How It Stacks Up

To determine if Kovo really works better than alternatives, I compared it to the top credit building services:

Why Kovo Wins for Most People

Kovo’s advantages:

- 4 credit bureau reporting (vs 2-3 for competitors)

- Lower minimum payment ($10 vs $15-25)

- Highest customer satisfaction (4.9/5 stars)

- Best mobile app experience

- Transparent 24-month timeline

When competitors might be better:

- Kik off: If you want the absolute lowest cost ($5/month)

- Self: If you prefer a savings component

- Credit Strong: If you want the shortest program (12 months)

Who Should (and Shouldn’t) Use Kovo

Kovo Is Perfect For:

✅ Complete Credit Beginners

- 18-25 year olds with no credit history

- New immigrants to the US

- People who’ve never had credit cards or loans

✅ Credit Rebuilders

- After bankruptcy or major financial setbacks

- Recovering from damaged credit

- Want guaranteed approval regardless of past

✅ Budget-Conscious Users

- Can afford $10-25/month consistently

- Want predictable, no-surprise costs

- Prefer transparency over complicated fee structures

✅ Tech-Savvy Users

- Appreciate clean, modern mobile apps

- Want to track progress digitally

- Prefer online account management

Kovo Might Not Be Right For:

❌ People With Existing Good Credit

- If you already have 650+ credit score

- Better to focus on optimizing existing accounts

- Credit builder accounts won’t help much

❌ Those Wanting Immediate Access to Money

- Kovo doesn’t provide spending money or loans

- Consider secured credit cards if you need purchasing power

- Not a solution for immediate financial needs

❌ Extremely Tight Budgets

- If $10/month is a financial strain

- Consider free alternatives like becoming an authorized user

- Focus on increasing income first

Kovo Pros and Cons: The Complete Truth

The Good: Why Kovo Works

✅ Guaranteed Approval No credit check means 100% acceptance rate. Perfect for people who’ve been denied everywhere else.

✅ Reports to All 4 Credit Bureaus Most services only report to 3 bureaus. Kovo includes Innovis (the 4th bureau) for maximum coverage.

✅ Affordable and Transparent $10/month minimum with no hidden fees, interest charges, or surprise costs.

✅ User-Friendly Experience Clean mobile app, easy account management, and helpful customer service.

✅ Proven Results Thousands of users have successfully built credit from 0 to 700+ scores.

The Not-So-Good: Honest Drawbacks

Takes Time Results aren’t instant – expect 2-3 months for first score, 6+ months for significant improvements.

Monthly Commitment Requires consistent payments for 24 months. Missing payments defeats the purpose.

No Immediate Spending Power Unlike credit cards, you can’t use Kovo to make purchases.

Limited Advanced Features Basic credit building only no rewards, cash back, or additional perks.

24-Month Commitment Longer than some competitors who offer 12-month programs.

How to Get Started with Kovo

Ready to see if Kovo works for you? Here’s exactly how to get started:

Step 1: Sign Up (2 Minutes)

- Visit Kovo’s website using our link below

- Enter basic information (name, address, phone, email)

- Choose monthly payment ($10, $15, $20, or $25)

- Set up payment method (bank account or debit card)

- Confirm and start building credit immediately

No credit check, no waiting period, no rejection risk.

Step 2: Set Up Automatic Payments

- Link your checking account for automatic monthly payments

- Choose payment date that works with your budget

- Enable notifications to track your progress

Step 3: Monitor Your Progress

- Download Credit Karma (free) to track score improvements

- Check Kovo app monthly to see payment history

- Celebrate milestones as your credit score grows

Step 4: Plan Your Next Steps

- Month 6: Apply for your first credit card

- Month 12: Consider additional credit building strategies

- Month 24: Graduate to premium credit products

Ready to Start Building Credit Today?

Join thousands of users who’ve successfully built credit with Kovo.

✅ No credit check required

✅ Guaranteed approval

✅ Only $10/month to start

✅ Reports to all 4 credit bureaus

✅ 4.9-star rating from real users

GET STARTED WITH KOVO – NO CREDIT CHECK REQUIRED

Start building the credit score you deserve in just 2 minutes.

Frequently Asked Questions

Does Kovo actually work to build credit?

Yes, Kovo works by reporting your monthly payments to all 4 credit bureaus (Experian, Equifax, TransUnion, and Innovis). Users typically see their first credit score within 2-3 months and average improvements of 40-60 points in the first year.

How long does it take to see results with Kovo?

Timeline for results:

- Month 1-2: Credit file established

- Month 3: First credit score appears (usually 580-620)

- Month 6: Significant improvement (620-680 range)

- Month 12: Good credit territory (680-740)

- Month 24: Excellent credit potential (720-780+)

Is Kovo better than other credit builders?

- Reports to 4 credit bureaus (vs 2-3 for competitors)

- Has the lowest minimum payment ($10/month)

- Offers guaranteed approval with no credit check

- Has the highest customer satisfaction rating (4.9/5 stars)

What happens if I miss a Kovo payment?

Missing payments defeats the purpose of credit building. Kovo may report late payments to credit bureaus, which could hurt your credit score. Always set up automatic payments to avoid this risk.

Can I cancel Kovo early?

Yes, you can cancel anytime, but you’ll get the best results by completing the full 24-month program. Early cancellation means less credit history and potentially lower score improvements.

Will Kovo help me get approved for credit cards?

Yes, many users report getting approved for their first credit cards after 3-6 months with Kovo. The payment history and established credit file make you more attractive to lenders.

Does Kovo cost anything besides the monthly payment?

No, Kovo has no hidden fees, setup costs, or interest charges. The monthly payment ($10-25) is the only cost.

Is Kovo safe and legitimate?

Yes, Kovo is a legitimate financial service that’s fully compliant with credit reporting regulations. They use bank-level security and have thousands of positive user reviews.

Can I use Kovo if I have bad credit?

Yes, Kovo accepts users regardless of credit history, including those with bad credit, no credit, or past bankruptcies. There’s no credit check for approval.

What credit score can I expect with Kovo?

Results vary, but most users see:

- 580-620 after 3 months (first score)

- 620-680 after 6 months

- 680-740 after 12 months

- 720+ after 24 months (with good habits)

Final Verdict: Does Kovo Work?

Bottom line: Yes, Kovo absolutely works for building credit.

After testing Kovo personally and analyzing hundreds of user reviews, the evidence is clear: Kovu consistently helps people build credit from scratch or recover from financial setbacks.

Why Kovo Works So Well

- Scientific approach: Reports to all 4 credit bureaus for maximum impact

- Consistency: 24-month program builds substantial payment history

- Accessibility: No credit check means anyone can start

- Affordability: $10/month makes it accessible to most budgets

- User experience: Simple app and process encourage consistency

Is Kovo Worth It?

For most people starting their credit journey: Absolutely.

At $10/month ($240 total), Kovo costs less than:

- One late payment fee on a credit card

- A single month of high interest charges

- The security deposit on most secured credit cards

The return on investment is enormous when you consider:

- Lower interest rates on future loans

- Better credit card approvals and rewards

- Lower insurance premiums

- Better rental applications

- Improved financial confidence

My Recommendation

Start with Kovo if you:

- Have no credit score or poor credit

- Want guaranteed approval

- Can commit to 24 months of payments

- Prefer a simple, straightforward approach

Consider alternatives if you:

- Already have good credit (650+)

- Need immediate access to spending money

- Can’t afford $10/month consistently

The question isn’t really does Kovo work? are you ready to commit to building better credit?

If you’re ready to take control of your financial future, Kovo provides a proven, affordable path to excellent credit.

Start Building Credit Today Zero Risk

Ready to join thousands of successful Kovo users?

✅ No credit check – 100% approval guaranteed

✅ Just $10/month – cancel anytime

✅ See results in 2-3 months – first score appears fast

✅ 4.9-star rating – proven track record

✅ Reports to 4 bureaus – maximum credit impact

Don’t wait every month you delay is a month of missed credit building.

START YOUR KOVO CREDIT JOURNEY NOW

Join the thousands who’ve transformed their financial lives with Kovo.

About the Author: I’m a personal finance expert who’s helped hundreds of people build credit from scratch. After personally testing Kovo and researching dozens of alternatives, I provide honest, real-world advice based on actual results.

Disclaimer: This article contains affiliate links. We may earn a commission if you sign up for Kovo through our links, at no additional cost to you. All opinions and results shared are genuine and based on real user experiences.

Want more productivity tips like this?

Subscribe to our newsletter for weekly guides on digital tools that make your life easier.