Starting a new job is exciting but what happens when you need a personal loan before you’ve built up six months of employment history? Many lenders prefer borrowers with stable long term employment but don’t worry there are still ways to secure financing even with a shorter work history.

Why Employment History Matters to Lenders

Lenders view employment history as a key indicator of your ability to repay a loan. Traditionally they prefer seeing 6+ months of consistent income because it demonstrates job stability and reduces their risk. However, your situation isn’t hopeless if you’re new to your position.

5 Strategies to Get Approved with Short Employment History

1. Highlight Your Industry Experience

Even if you’re new to your current job emphasize your overall experience in the field. A career change within the same industry shows stability and expertise that lenders value.

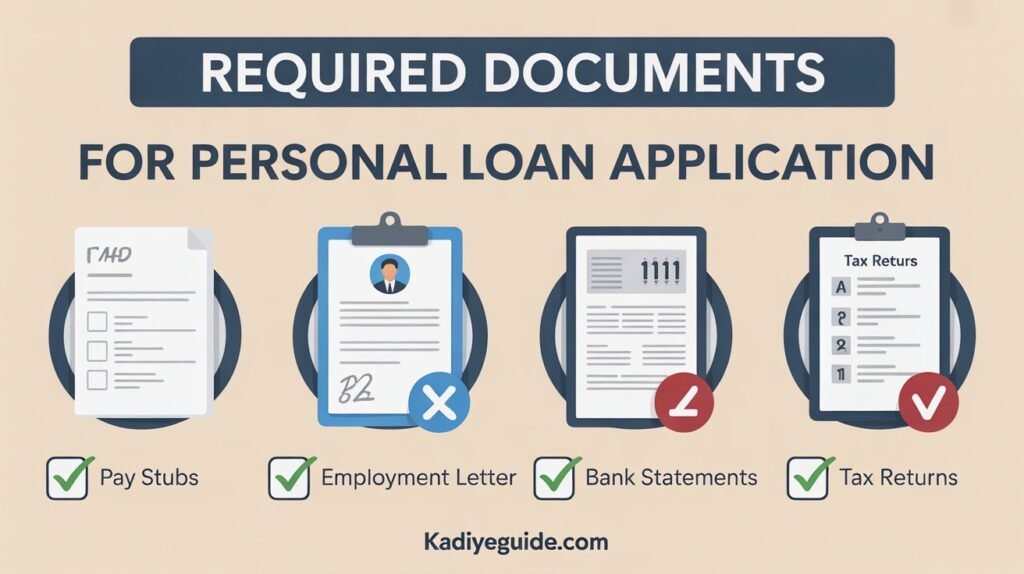

2. Provide Strong Income Documentation

Gather these documents to strengthen your application:

- Recent pay stubs 2-3 months minimum

- Employment offer letter with salary details

- Bank statements showing consistent deposits

- Tax returns from previous employment

3. Consider Co Signer Options

A co signer with good credit and stable income can significantly boost your approval chances. This person agrees to take responsibility for the loan if you can’t pay reducing the lender’s risk.

4. Start with Smaller Loan Amounts

Requesting a smaller loan amount increases your approval odds and demonstrates responsible borrowing. You can always apply for additional funding once you’ve established a payment history.

5. Shop Around with Multiple Lenders

Different lenders have varying requirements. Online lenders and credit unions often have more flexible employment criteria than traditional banks.

Ready to find your perfect personal loan? Compare rates from multiple lenders in just 2 minutes with PersonalLoans.com. Check your rate without affecting your credit score.

Best Lenders for New Employees

Some lenders are more accommodating to borrowers with shorter employment history:

- Online platforms like PersonalLoans.com connect you with multiple lenders

- Credit unions often consider your overall financial picture

- Peer to peer lenders may have flexible requirements

- Community banks sometimes prioritize local relationships over strict guidelines

What If You Get Denied?

Don’t panic if your first application is denied Consider these alternatives:

- Wait 2-3 months and reapply with more employment history

- Improve your credit score during the waiting period

- Explore secured loan options using collateral

- Ask family or friends for temporary assistance

Still have questions about qualifying? Let PersonalLoans.com match you with lenders who work with borrowers in your situation. Free pre qualification in minutes.

Frequently Asked Questions

Q: How many pay stubs do I need for a personal loan? A: Most lenders require 2-3 recent pay stubs, though some may accept just one if you provide additional income verification like an employment letter or bank statements.

Q: Can I get a personal loan during my probationary period? A: Yes, some lenders will consider applications from borrowers in probationary periods, especially if you can provide a signed employment contract and demonstrate stable income from previous jobs.

Q: Will my interest rate be higher with short employment history? A: Potentially, yes. Lenders may charge higher rates to offset the perceived risk of lending to someone with limited job stability. However, shopping around can help you find competitive rates.

Q: What’s the minimum employment time most lenders require? A: While many traditional lenders prefer 6+ months, some alternative lenders may approve loans with just 1-3 months of employment history, especially with strong credit scores.

Q: Should I wait to apply for a personal loan until I have more employment history? A: It depends on your urgency. If you can wait, building 3-6 months of employment history will improve your approval odds and potentially get you better rates. However, if you need funds urgently, applying now with proper documentation is worth trying.

Conclusion

Getting a personal loan with less than six months of employment is challenging but definitely possible. Focus on demonstrating income stability through comprehensive documentation, consider working with a co signer and shop around with multiple lenders to find the best fit for your situation.

Remember, even if you’re approved with shorter employment history, making on time payments will help build your credit and improve your borrowing power for future needs.

Ready to start your application? Visit PersonalLoans.com today to connect with lenders who understand your unique situation and get pre qualified in just minutes.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Rates and terms mentioned are estimates and may vary based on creditworthiness and lender requirements. Always compare multiple offers and read the fine print before applying.

Want more productivity tips like this?

Subscribe to our newsletter for weekly guides on digital tools that make your life easier.